-

What do you understand by the word insurance?

An agreement between a person or entity (the insured) and an insurance firm (the insurer) is known as insurance. In exchange for payment of a premium, the insurer agrees to provide financial protection or compensation to the insured for specified losses, damages, or liabilities covered under the terms of the insurance policy.

The purpose of insurance is to mitigate financial risk by transferring it from the insured to the insurer. The insured can shield themselves from the financial ramifications of unanticipated catastrophes, such as diseases, accidents, natural disasters, or liability claims, by paying a comparatively low premium.

The terms, conditions, coverage limitations, exclusions, and other specifics of the insurance arrangement are usually outlined in insurance policies. Some examples of common insurance categories are health, life, business, renters, homeowners, and vehicle insurance.

All things advised, insurance offers financial stability, peace of mind, and defense against unforeseen financial losses or hardships to individuals, families, companies, and other entities.

- Role of an insurance company?

An insurance company provides financial protection or reimbursement against specified losses or damages, typically in exchange for regular payments known as premiums. In principle, it divides up the risk of monetary loss across a group of policyholders. When individuals or businesses face unexpected events like accidents, illnesses, property damage, or other risks covered by their policy, the insurance company compensates them according to the terms of their policy.

- Describe insurance operations?

The different tasks and procedures that go into running an insurance company are together referred to as insurance operations. These operations typically include:

Underwriting: This involves assessing risks associated with potential policyholders and deciding whether to accept or reject their applications for insurance coverage.

Policy issuance: Once a policy is underwritten and approved, the insurance company issues the policy documents to the policyholder, outlining the terms, coverage limits, premiums, and other relevant details.

Premium collection: Insurance companies collect premiums from policyholders, either as a lump sum or through periodic payments, to maintain coverage.

Claims processing: When policyholders experience covered losses or damages, they file claims with the insurance company. The process of handling insurance claims include assessing them, judging their veracity, and allocating funds or benefits appropriately.

Risk management: Insurance companies employ risk management strategies to minimize potential losses and ensure their financial stability. Compromising reinsurance, diversifying the portfolio, and taking other steps to lower risk may be necessary for this.

Actuarial analysis: Actuaries play a crucial role in insurance operations by using statistical models and data analysis to assess risks, set premium rates, and determine appropriate reserves. Customer service: Insurance companies provide support to policyholders, agents, and other stakeholders through various customer service channels, including phone, email, and online platforms. Regulatory compliance: Insurance operations must adhere to regulations and standards set by regulatory bodies to ensure fair practices, financial solvency, and consumer protection.

Marketing and sales: Insurance companies engage in marketing and sales activities to attract new customers, promote their products, and expand their market presence.

Investment management: Insurance companies often invest premiums collected from policyholders to generate returns and support their financial operations. To stay solvent and fulfill commitments to policyholders, one must practice effective investment management.

- What is the most basic type of insurance?

The most basic type of insurance is typically considered to be term life insurance. Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years, and pays out a death benefit if the insured individual passes away during the term of the policy. It's straightforward in its structure, providing protection for a set period without any savings or investment components like whole life or universal life insurance. Term life insurance is often chosen for its simplicity and affordability, making it a popular choice for individuals seeking basic life insurance coverage.

- How many departments are in an insurance company?

The number of departments in an insurance company can vary depending on the size, structure, and scope of operations of the company. However, most insurance companies typically have several key departments, including:

- Underwriting: Responsible for assessing risks associated with potential policyholders and determining whether to accept or reject insurance applications.

- Claims: Handles the processing and settlement of claims filed by policyholders for covered losses or damages.

- Customer Service: Provides support to policyholders just like a family member and other stakeholders regarding policy inquiries, billing questions, and other related issues.

- Actuarial: Conducts statistical analysis and risk assessment to set premium rates, establish reserves, and ensure the financial stability of the company.

- Marketing and Sales: Develops strategies to attract new customers in all cities, promote insurance products, and expand market presence in india.

- Finance and Accounting: Manages financial transactions, budgeting, financial reporting, and other accounting functions.

- Human Resources: Handles recruitment, training, employee relations, and other personnel-related matters.

- Information Technology (IT): Maintains and manages the company's technology infrastructure, including software systems, networks, and data security.

- Legal and Compliance: Manages legal issues and regulatory compliance while making sure the business's activities obey to applicable laws, rules, and industry standards.

- Risk Management: Identifies, assesses, and manages risks to the company's operations, financial stability, and reputation.

Larger insurance firms might also include specialized divisions or departments that concentrate on business strategy, product development, investment management, reinsurance, and other topics. The specific departments and their functions can vary based on the insurance company's business model, target market, and strategic priorities.

- What are the three main types of life insurance?

The three main types of life insurance are follows below:

- Term Life Insurance: This type of insurance provides coverage for a specified period, such as 10, 20, or 30 years. If the insured individual dies during the term, the beneficiaries receive the death benefit. However, if the insured survives the term, there is no payout at the end of the policy.

- Whole Life Insurance: Whole life insurance provides coverage for the entire lifetime of the insured, as long as premiums are paid. It also includes a savings component called cash value, which grows over time and can be borrowed against or withdrawn by the policyholder. Whole life insurance typically offers fixed premiums and a guaranteed death benefit.

- Universal Life Insurance: Universal life insurance is similar to whole life insurance but offers more flexibility. Policyholders can adjust the premium payments and death benefits over time, within certain limits. Universal life insurance also includes a cash value component, but the interest rates and premiums may vary depending on market conditions.

- What are the top 3 types of insurance?

The top three types of insurance, in terms of their importance and widespread usage, are:

- Health Insurance: Health insurance provides coverage for medical expenses incurred due to illness, injury, or preventive care. It gives all services, including as doctor visits, hospital stays, prescription drugs, and medical treatments, more facilities for people and families. Health insurance can be obtained through employers, government programs (such as Medicare or Medicaid), or purchased individually.

- Vehicle Insurance: Vehicle insurance provides financial protection against physical damage and bodily injury resulting from accidents involving vehicles. It typically includes coverage for property damage liability, bodily injury liability, collision, comprehensive, and uninsured/underinsured motorist coverage. Vehivle insurance is mandatory in every states and is essential for protecting both drivers and their vehicles.

- Life Insurance: Life insurance offers financial protection to beneficiaries in the event of the insured individual's death. It provides a lump-sum payment, known as the death benefit, to designated beneficiaries upon the death of the insured. Life insurance may assist with debt repayment, burial costs, income replacement, and providing stability for dependents financially. Term life, whole life, and universal life insurance are among the several kinds of life insurance plans.

Health, Vehicle, and life insurance are the three main categories of insurance that are seen to be necessary for the safety of people and families, and their all people in the world.

- What are the 3 levels of insurance?

The three levels of insurance coverage commonly referred to are:

- Basic Coverage: Basic coverage typically refers to the minimum amount of insurance required by law or necessary to meet essential needs. For example, in auto insurance, basic coverage might include liability coverage to cover damages and injuries caused to others in an accident where you're at fault. Basic coverage is often the most affordable option but may not provide comprehensive protection.

- Standard Coverage: Standard coverage offers a more comprehensive level of protection compared to basic coverage. It's includes a wider range of benefits and higher coverage limits. For instance, in auto insurance, standard coverage might include liability coverage, collision coverage to pay for damages to your vehicle in an accident, and comprehensive coverage for non-collision incidents like theft or vandalism.

- Premium Coverage: Premium coverage provides the highest level of protection and often includes additional benefits or features beyond what's offered in standard coverage. Although the premiums for this level of coverage are higher, they provide more financial stability and peace of mind in later life. In auto insurance, premium coverage might include higher liability limits, additional coverage for rental car reimbursement, roadside assistance, and other perks.

- Describe 5 disadvantages of insurance?

While insurance provides essential financial protection, there are also some potential disadvantages associated with it:

- Cost: Insurance premiums can be costly, especially for comprehensive coverage or policies with high coverage limits. Paying premiums regularly can strain your budget, and if you don't make claims, it may feel like you're not getting tangible benefits in return.

- Coverage Limitations: Insurance policies often come with limitations and exclusions, meaning certain events or circumstances may not be covered. while filing a claim understanding these limitations is crucial to avoid surprises.

- Deductibles and Co-Payments: Prior to the start of coverage, policyholders of many insurance plans must make deductibles or co-payments. These cash outlays may mount up, especially if you have to submit claims on a regular basis.

- Administrative Hassles: Dealing with insurance paperwork, filing claims, and communicating with insurance companies can be time-consuming and sometimes frustrating. Handling the claims procedure can be difficult, particularly if disagreements emerge over coverage or the amount of the claim.

- Over-reliance: Relying too heavily on insurance coverage may lead to complacency and a lack of proactive risk management. It's critical to keep in mind that insurance may not be able to stop accidents or natural catastrophes from happening, but it is intended to lessen financial damages. It's dangerous to continue taking a balanced approach to risk management.

While these disadvantages exist, the benefits of insurance—financial protection, peace of mind, and risk mitigation—often outweigh the drawbacks for most individuals and businesses.

- What do you mean by insurer?

An insurer is a advisor that provides insurance coverage to individuals, business man, or other organizations in return for premium payments. Typically, this organization is an insurance company or a reinsurer. The financial risk related to any losses covered by the insurance policies it offers is assumed by the insurer.

An insurer's primary duties and obligations include:

- Underwriting: Insurers assess the risk profile of prospective policyholders to determine the appropriate premiums and coverage limits. Evaluations of the insured's health, driving history, property worth, and other pertinent data are part of this procedure.

- Issuing Policies: Insurers issue insurance policies to policyholders, outlining the terms, conditions, coverage limits, exclusions, and other details of the insurance agreement.

- Collecting Premiums: Insurers collect premiums from policyholders in exchange for providing insurance coverage. Premiums are typically paid regularly, such as monthly, quarterly, or annually.

- Managing Risk: Insurers use actuarial and risk management techniques to assess and manage the financial risks associated with providing insurance coverage. This means choosing suitable premium levels, distributing risk over a variety of policies, and keep sufficient reserves to cover claims in the future.

- Processing Claims: Insurers handle claims submitted by policyholders in accordance with the terms of their insurance policies. Claims investigation, eligibility for coverage determination, and policyholder reimbursement for insured losses or damages are all part of this process.

- Providing Customer Service: Insurers offer customer support services to policyholders, including assistance with policy inquiries, billing questions, claims processing, and other related matters.

Providers of financial protection and assurance to individuals, businesses, and other organizations that could be subject to risks and uncertainties, insurers are, in general, indispensable to the insurance industry.

- Describe premium insurance?

"Premium insurance" isn't a standard term in the insurance industry. However, it's possible that you might be referring to two different concepts related to insurance:

- Premium Payments: In insurance, a "premium" refers to the amount of money that an individual or business pays to an insurance company in exchange for coverage. The frequency of premium payments, such as monthly or yearly, depends on a number of criteria, including the kind of insurance, coverage limits, deductible amount, risk profile of the insured party, and other pertinent information.

- Premium Coverage: Sometimes, "premium insurance" might be used colloquially to refer to insurance policies that offer high levels of coverage or additional benefits beyond basic or standard insurance plans. We offer more safety or extra features, such as increased coverage limits, a wider range of coverage, or other benefits like travel insurance or roadside assistance because these premium insurance plans frequently have higher premiums.

If you have a specific context or type of insurance in mind when referring to "premium insurance," feel free to provide more details, and I can offer a more tailored explanation.

- Write the main principles of insurance?

The main principles of insurance are:

- Principle of Utmost Good Faith (Uberrimae Fidei): Both the insured and the insurer are required to act in good faith and provide complete and accurate information to each other. In the insurance contract, this idea shows that it is very transparent and honest in the design and execution.

- Principle of Insurable Interest: The insured must have a financial interest in the subject matter of the insurance policy. This means that the insured must suffer a financial loss if the insured event occurs. Insurance contracts can't be utilized for speculation or gambling thanks to insurable interest.

- Principle of Indemnity: The principle of indemnity states that the insured should not profit from an insurance claim but should be restored to the same financial position they were in before the loss occurred. Insurance compensation is designed to compensate for the actual financial loss suffered, up to the limit of the policy.

- Principle of Contribution: If the insured has multiple insurance policies covering the same risk, each insurer will contribute proportionately to the loss. This principle prevents the insured from collecting more than the actual loss from multiple insurance policies, known as over-insurance.

- Principle of Subrogation: When an insurance company pays a claim to the insured, it gains the right to pursue legal action against any third party responsible for the loss. Subrogation allows the insurer to recover the amount paid to the insured and helps prevent the insured from collecting double compensation for the same loss.

- Principle of Loss Minimization: The insured has a duty to take reasonable steps to minimize the extent of the loss after an insured event occurs. If damages are not mitigated, the insurance provider may offer you less money.

These guiding ideas promote equality, accountability, and transparency in the insurance business By acting as the cornerstone of insurance contracts and a framework for interactions between insurers and insured parties.

- What is 4 and 8 in insurance?

In the insurance industry, "4 and 8" typically refers to the rule regarding payment of insurance premiums. It's more commonly known as the "Four and Eight Payment Plan."

The Four and Eight Payment Plan allows policyholders to pay their insurance premiums in installments, usually over four or eight equal payments. Policyholders who would rather not pay the full premium at once and instead spread it out over many months can do so with this arrangement, which provides flexibility.

For example, if an insurance policy has an annual premium of ,200, under the Four and Eight Payment Plan, the policyholder could pay it in four equal installments of 0 each or in eight equal installments of 0 each.

This payment plan is frequently available for a number of insurance policies, including renters', homeowners', and vehicle insurance. While preserving their insurance coverage it supports policyholders in efficiently managing their cash flow and spending plans.

- What is three types of insurers?

There are several kinds of insurers in the insurance business, and they all cater to distinct market niches and provide distinct kinds of insurance goods. Here are three common types of insurers:

- Stock Insurance Companies: Stock insurance companies are owned by shareholders who invest in the company's stock. When the business is making profit then the Shareholder gets return profits. Policyholders typically do not have ownership rights in the company. Property and casualty insurance, health insurance, life insurance, and other insurance products are just a few of the many products that stock insurance firms may provide.

- Mutual Insurance Companies: Mutual insurance companies are owned by their policyholders rather than external shareholders. Policyholders are considered members of the mutual company and may have voting rights and participate in the company's governance. Mutual insurers operate on a not-for-profit basis, with any profits generated being returned to policyholders in the form of dividends, lower premiums, or enhanced benefits. Mutual insurance companies often focus on providing life insurance, property and casualty insurance, or specialized insurance products.

- Reciprocal Insurance Exchanges: Reciprocal insurance exchanges, also known as interinsurance exchanges or reciprocal insurers, are unincorporated groups of individuals or entities that collectively insure each other's risks. Policyholders in a reciprocal insurance exchange pool their resources to provide insurance coverage to each other. Each policyholder is both an insured and an insurer, sharing in the risk and rewards of the exchange. Different kinds of insurance coverage, including liability, professional indemnity, and property and casualty insurance, may be available through reciprocal insurance exchanges.

These are only the three most typical kinds of insurance, but there are other variations and structures within the insurance industry, including captive insurance companies, government insurers, and reinsurance companies, among others. These are the type of insurance which has unique characteristics, advantages, and legal considerations.

- What are the 6 rules of insurance?

While there isn't a standard set of "6 rules of insurance," the principles and guidelines governing insurance are often summarized into several key principles or rules. Here's a compilation of six essential rules or principles of insurance:

- Utmost Good Faith (Uberrimae Fidei): Both the insured and the insurer are required to act in utmost good faith and provide complete and accurate information to each other during the formation and execution of the insurance contract. This idea guarantees openness, truthfulness, and justice in the insurance relationship.

- Insurable Interest: The insured must have a legitimate financial interest in the subject matter of the insurance policy. Insurable interest ensures that the insured would suffer a financial loss if the insured event occurs, preventing insurance contracts from being used for speculative purposes.

- Indemnity: The principle of indemnity states that insurance compensation should only cover the actual financial loss suffered by the insured, up to the limit of the policy. Insurance is intended to restore the insured to the same financial position they were in before the loss occurred, without allowing them to profit from the insurance claim.

- Contribution: If the insured has multiple insurance policies covering the same risk, each insurer will contribute proportionately to the loss. This principle prevents the insured from receiving more than the actual loss from multiple insurance policies, known as over-insurance.

- Subrogation: When an insurance company pays a claim to the insured, it gains the right to pursue legal action against any third party responsible for the loss. Subrogation allows the insurer to recover the amount paid to the insured and prevents the insured from collecting double compensation for the same loss.

- Mitigation of Loss: The insured has a duty to take reasonable steps to minimize the extent of the loss after an insured event occurs. If damages are not mitigated, the insurance provider may offer you less money.

These rules and principles form the foundation of insurance contracts and govern the relationship between insurers and insured parties, ensuring fairness, transparency, and accountability in the insurance industry.

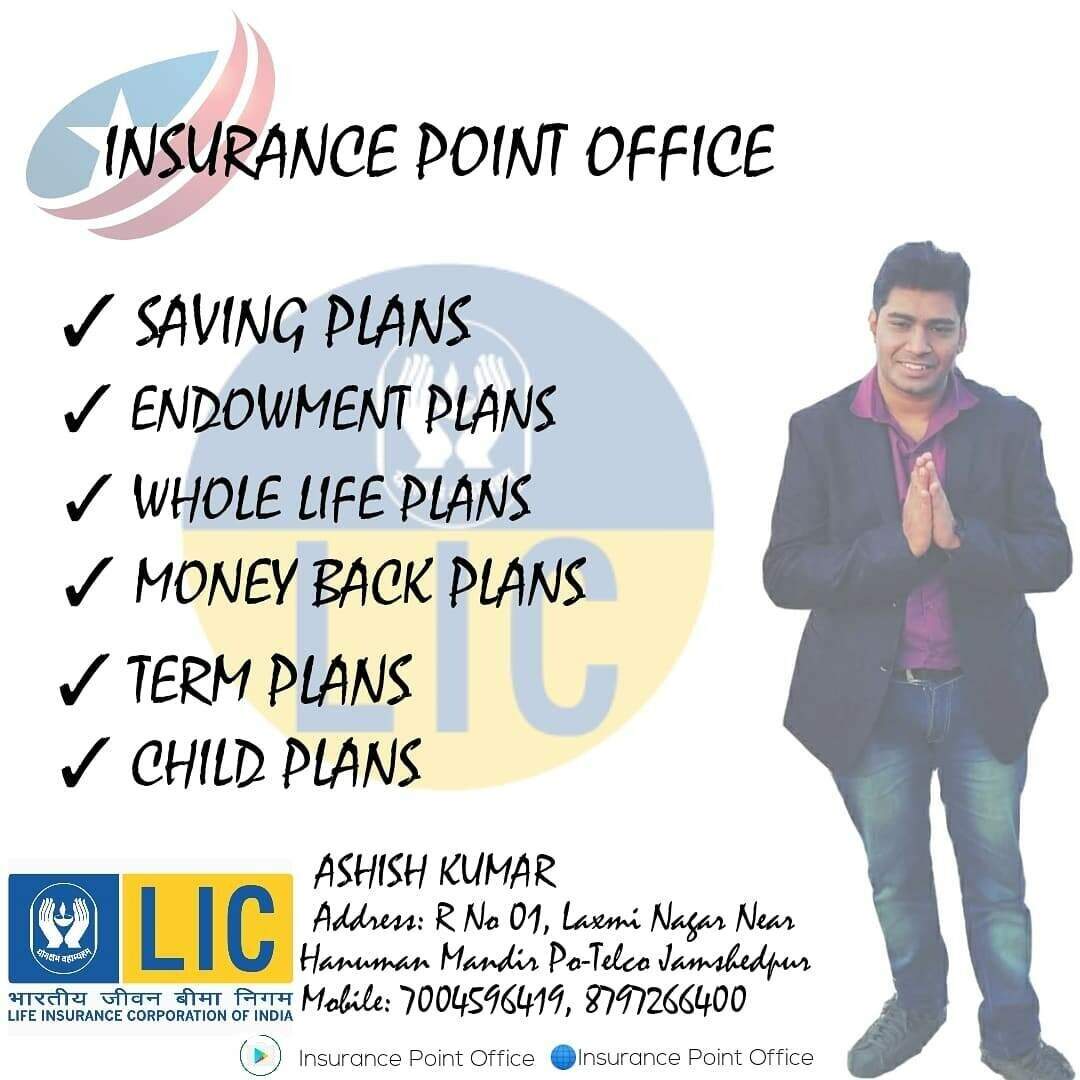

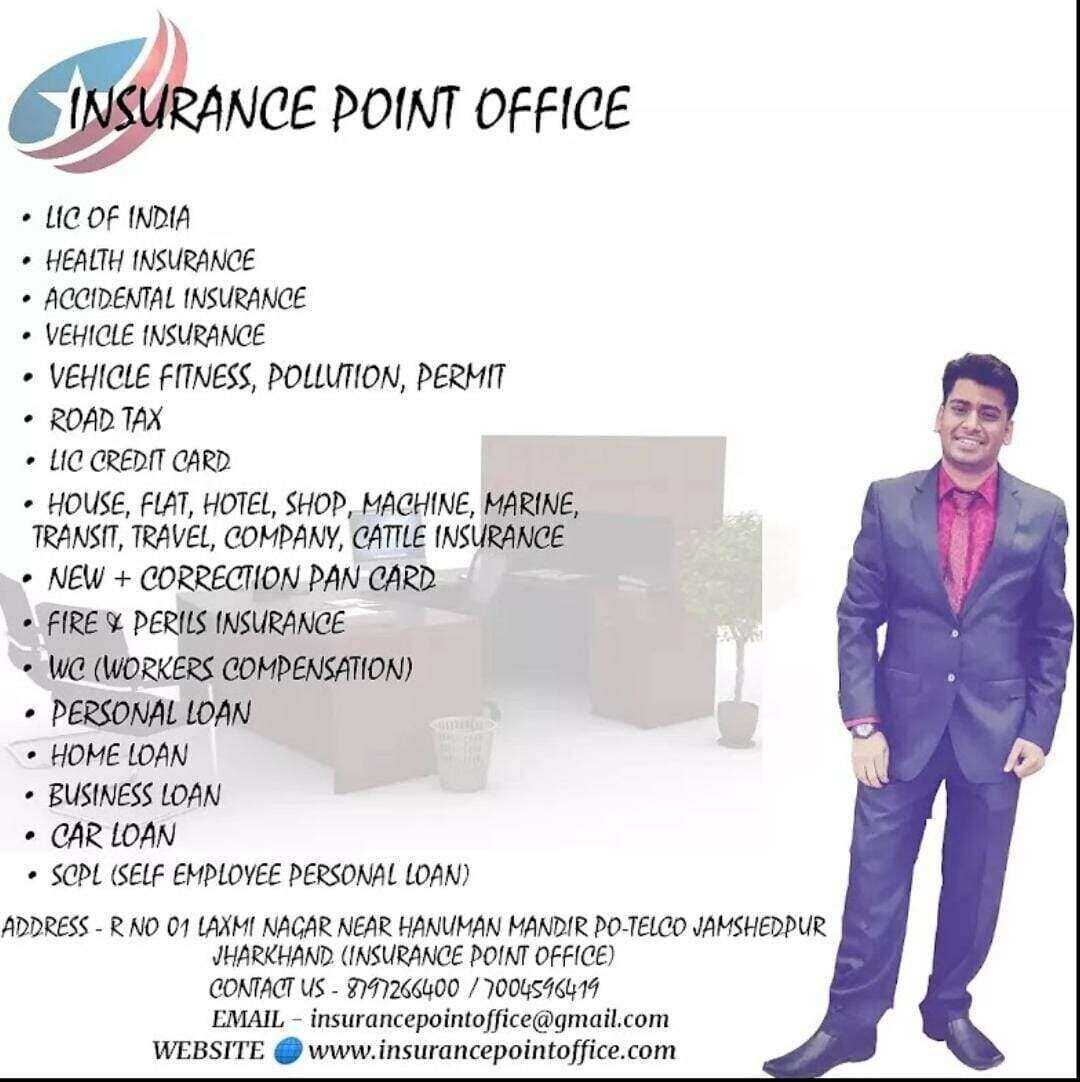

Written By - Insurance Point Office