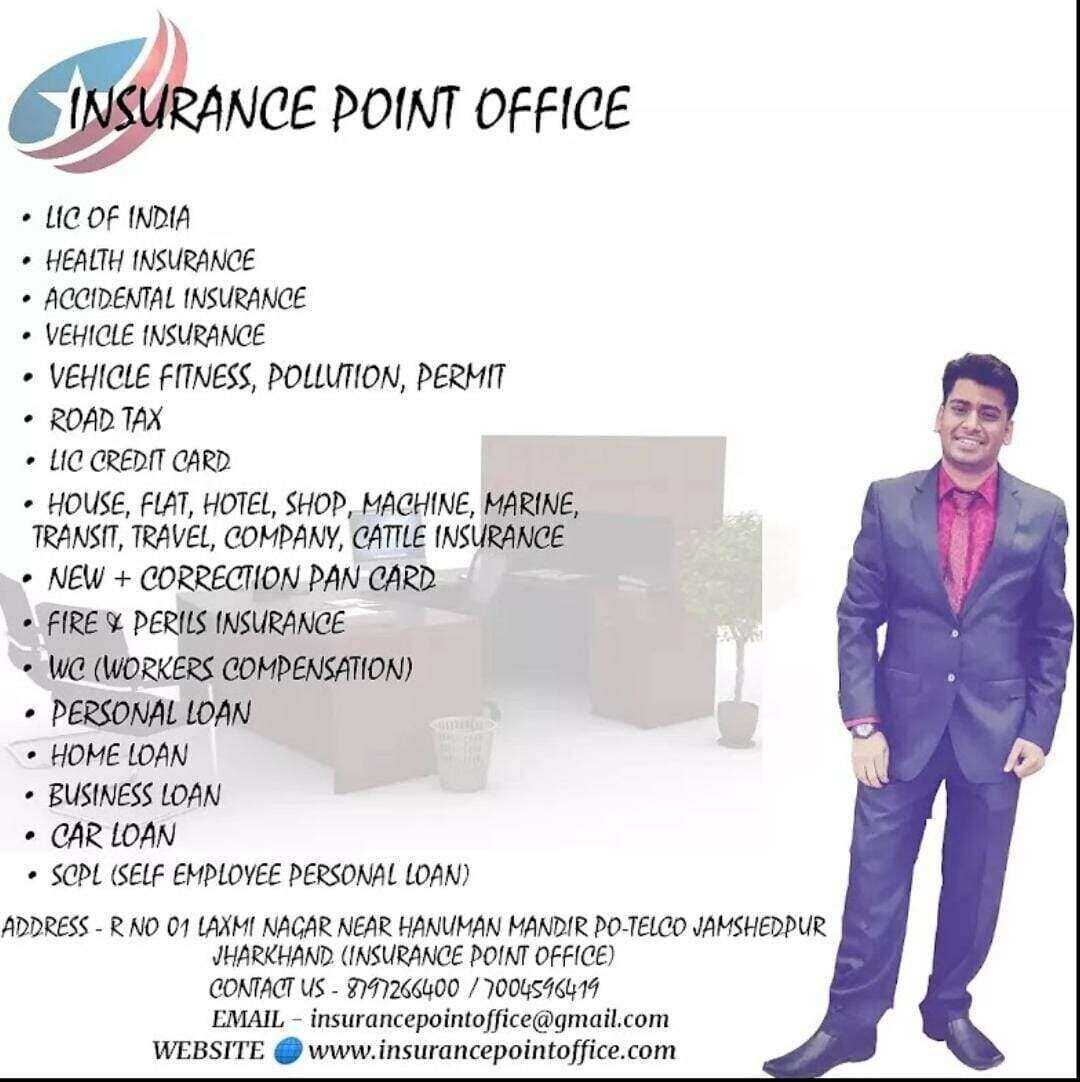

BLOGS

Created on 26 dec 2023 - Insurance

Why insurance is needed in your daily life

-

What do you understand by the word insurance?

An agreement between a person or entity (the insured) and an insurance firm (the insurer) is known as insurance. In exchange for payment of a premium, the insurer agrees to provide financial protection or compensation to the insured for specified losses, damages, or liabilities covered under the terms of the insurance policy.

The purpose of insurance is to mitigate financial risk by transferring it from the insured to the insurer. The insured can shield themselves from the financial ramifications of unanticipated catastrophes, such as diseases, accidents, natural disasters, or liability claims, by paying a comparatively low premium.

The terms, conditions, coverage limitations, exclusions, and other specifics of the insurance arrangement are usually outlined in insurance policies. Some examples of common insurance categories are health, life, business, renters, homeowners, and vehicle insurance.

All things advised, insurance offers financial stability, peace of mind, and defense against unforeseen financial losses or hardships to individuals, families, companies, and other entities.

- Role of an insurance company?

An insurance company provides financial protection or reimbursement against specified losses or damages, typically in exchange for regular payments known as premiums. In principle, it divides up the risk of monetary loss across a group of policyholders. When individuals or businesses face unexpected events like accidents, illnesses, property damage, or other risks covered by their policy, the insurance company compensates them according to the terms of their policy.

- Describe insurance operations?

The different tasks and procedures that go into running an insurance company are together referred to as insurance operations. These operations typically include:

Underwriting: This involves assessing risks associated with potential policyholders and deciding whether to accept or reject their applications for insurance coverage.

Policy issuance: Once a policy is underwritten and approved, the insurance company issues the policy documents to the policyholder, outlining the terms, coverage limits, premiums, and other relevant details.

Premium collection: Insurance companies collect premiums from policyholders, either as a lump sum or through periodic payments, to maintain coverage.

Claims processing: When policyholders experience covered losses or damages, they file claims with the insurance company. The process of handling insurance claims include assessing them, judging their veracity, and allocating funds or benefits appropriately.

Risk management: Insurance companies employ risk management strategies to minimize potential losses and ensure their financial stability. Compromising reinsurance, diversifying the portfolio, and taking other steps to lower risk may be necessary for this.

Actuarial analysis: Actuaries play a crucial role in insurance operations by using statistical models and data analysis to assess risks, set premium rates, and determine appropriate reserves. Customer service: Insurance companies provide support to policyholders, agents, and other stakeholders through various customer service channels, including phone, email, and online platforms. Regulatory compliance: Insurance operations must adhere to regulations and standards set by regulatory bodies to ensure fair practices, financial solvency, and consumer protection.

Marketing and sales: Insurance companies engage in marketing and sales activities to attract new customers, promote their products, and expand their market presence.

Investment management: Insurance companies often invest premiums collected from policyholders to generate returns and support their financial operations. To stay solvent and fulfill commitments to policyholders, one must practice effective investment management.

- What is the most basic type of insurance?

The most basic type of insurance is typically considered to be term life insurance. Term life insurance provides coverage for a specific period, such as 10, 20, or 30 years, and pays out a death benefit if the insured individual passes away during the term of the policy. It's straightforward in its structure, providing protection for a set period without any savings or investment components like whole life or universal life insurance. Term life insurance is often chosen for its simplicity and affordability, making it a popular choice for individuals seeking basic life insurance coverage.

- How many departments are in an insurance company?

The number of departments in an insurance company can vary depending on the size, structure, and scope of operations of the company. However, most insurance companies typically have several key departments, including:

- Underwriting: Responsible for assessing risks associated with potential policyholders and determining whether to accept or reject insurance applications.

- Claims: Handles the processing and settlement of claims filed by policyholders for covered losses or damages.

- Customer Service: Provides support to policyholders just like a family member and other stakeholders regarding policy inquiries, billing questions, and other related issues.

- Actuarial: Conducts statistical analysis and risk assessment to set premium rates, establish reserves, and ensure the financial stability of the company.

- Marketing and Sales: Develops strategies to attract new customers in all cities, promote insurance products, and expand market presence in india.

- Finance and Accounting: Manages financial transactions, budgeting, financial reporting, and other accounting functions.

- Human Resources: Handles recruitment, training, employee relations, and other personnel-related matters.

- Information Technology (IT): Maintains and manages the company's technology infrastructure, including software systems, networks, and data security.

- Legal and Compliance: Manages legal issues and regulatory compliance while making sure the business's activities obey to applicable laws, rules, and industry standards.

- Risk Management: Identifies, assesses, and manages risks to the company's operations, financial stability, and reputation.

Larger insurance firms might also include specialized divisions or departments that concentrate on business strategy, product development, investment management, reinsurance, and other topics. The specific departments and their functions can vary based on the insurance company's business model, target market, and strategic priorities.

- What are the three main types of life insurance?

The three main types of life insurance are follows below:

- Term Life Insurance: This type of insurance provides coverage for a specified period, such as 10, 20, or 30 years. If the insured individual dies during the term, the beneficiaries receive the death benefit. However, if the insured survives the term, there is no payout at the end of the policy.

- Whole Life Insurance: Whole life insurance provides coverage for the entire lifetime of the insured, as long as premiums are paid. It also includes a savings component called cash value, which grows over time and can be borrowed against or withdrawn by the policyholder. Whole life insurance typically offers fixed premiums and a guaranteed death benefit.

- Universal Life Insurance: Universal life insurance is similar to whole life insurance but offers more flexibility. Policyholders can adjust the premium payments and death benefits over time, within certain limits. Universal life insurance also includes a cash value component, but the interest rates and premiums may vary depending on market conditions.

- What are the top 3 types of insurance?

The top three types of insurance, in terms of their importance and widespread usage, are:

- Health Insurance: Health insurance provides coverage for medical expenses incurred due to illness, injury, or preventive care. It gives all services, including as doctor visits, hospital stays, prescription drugs, and medical treatments, more facilities for people and families. Health insurance can be obtained through employers, government programs (such as Medicare or Medicaid), or purchased individually.

- Vehicle Insurance: Vehicle insurance provides financial protection against physical damage and bodily injury resulting from accidents involving vehicles. It typically includes coverage for property damage liability, bodily injury liability, collision, comprehensive, and uninsured/underinsured motorist coverage. Vehivle insurance is mandatory in every states and is essential for protecting both drivers and their vehicles.

- Life Insurance: Life insurance offers financial protection to beneficiaries in the event of the insured individual's death. It provides a lump-sum payment, known as the death benefit, to designated beneficiaries upon the death of the insured. Life insurance may assist with debt repayment, burial costs, income replacement, and providing stability for dependents financially. Term life, whole life, and universal life insurance are among the several kinds of life insurance plans.

Health, Vehicle, and life insurance are the three main categories of insurance that are seen to be necessary for the safety of people and families, and their all people in the world.

- What are the 3 levels of insurance?

The three levels of insurance coverage commonly referred to are:

- Basic Coverage: Basic coverage typically refers to the minimum amount of insurance required by law or necessary to meet essential needs. For example, in auto insurance, basic coverage might include liability coverage to cover damages and injuries caused to others in an accident where you're at fault. Basic coverage is often the most affordable option but may not provide comprehensive protection.

- Standard Coverage: Standard coverage offers a more comprehensive level of protection compared to basic coverage. It's includes a wider range of benefits and higher coverage limits. For instance, in auto insurance, standard coverage might include liability coverage, collision coverage to pay for damages to your vehicle in an accident, and comprehensive coverage for non-collision incidents like theft or vandalism.

- Premium Coverage: Premium coverage provides the highest level of protection and often includes additional benefits or features beyond what's offered in standard coverage. Although the premiums for this level of coverage are higher, they provide more financial stability and peace of mind in later life. In auto insurance, premium coverage might include higher liability limits, additional coverage for rental car reimbursement, roadside assistance, and other perks.

- Describe 5 disadvantages of insurance?

While insurance provides essential financial protection, there are also some potential disadvantages associated with it:

- Cost: Insurance premiums can be costly, especially for comprehensive coverage or policies with high coverage limits. Paying premiums regularly can strain your budget, and if you don't make claims, it may feel like you're not getting tangible benefits in return.

- Coverage Limitations: Insurance policies often come with limitations and exclusions, meaning certain events or circumstances may not be covered. while filing a claim understanding these limitations is crucial to avoid surprises.

- Deductibles and Co-Payments: Prior to the start of coverage, policyholders of many insurance plans must make deductibles or co-payments. These cash outlays may mount up, especially if you have to submit claims on a regular basis.

- Administrative Hassles: Dealing with insurance paperwork, filing claims, and communicating with insurance companies can be time-consuming and sometimes frustrating. Handling the claims procedure can be difficult, particularly if disagreements emerge over coverage or the amount of the claim.

- Over-reliance: Relying too heavily on insurance coverage may lead to complacency and a lack of proactive risk management. It's critical to keep in mind that insurance may not be able to stop accidents or natural catastrophes from happening, but it is intended to lessen financial damages. It's dangerous to continue taking a balanced approach to risk management.

While these disadvantages exist, the benefits of insurance—financial protection, peace of mind, and risk mitigation—often outweigh the drawbacks for most individuals and businesses.

- What do you mean by insurer?

An insurer is a advisor that provides insurance coverage to individuals, business man, or other organizations in return for premium payments. Typically, this organization is an insurance company or a reinsurer. The financial risk related to any losses covered by the insurance policies it offers is assumed by the insurer.

An insurer's primary duties and obligations include:

- Underwriting: Insurers assess the risk profile of prospective policyholders to determine the appropriate premiums and coverage limits. Evaluations of the insured's health, driving history, property worth, and other pertinent data are part of this procedure.

- Issuing Policies: Insurers issue insurance policies to policyholders, outlining the terms, conditions, coverage limits, exclusions, and other details of the insurance agreement.

- Collecting Premiums: Insurers collect premiums from policyholders in exchange for providing insurance coverage. Premiums are typically paid regularly, such as monthly, quarterly, or annually.

- Managing Risk: Insurers use actuarial and risk management techniques to assess and manage the financial risks associated with providing insurance coverage. This means choosing suitable premium levels, distributing risk over a variety of policies, and keep sufficient reserves to cover claims in the future.

- Processing Claims: Insurers handle claims submitted by policyholders in accordance with the terms of their insurance policies. Claims investigation, eligibility for coverage determination, and policyholder reimbursement for insured losses or damages are all part of this process.

- Providing Customer Service: Insurers offer customer support services to policyholders, including assistance with policy inquiries, billing questions, claims processing, and other related matters.

Providers of financial protection and assurance to individuals, businesses, and other organizations that could be subject to risks and uncertainties, insurers are, in general, indispensable to the insurance industry.

- Describe premium insurance?

"Premium insurance" isn't a standard term in the insurance industry. However, it's possible that you might be referring to two different concepts related to insurance:

- Premium Payments: In insurance, a "premium" refers to the amount of money that an individual or business pays to an insurance company in exchange for coverage. The frequency of premium payments, such as monthly or yearly, depends on a number of criteria, including the kind of insurance, coverage limits, deductible amount, risk profile of the insured party, and other pertinent information.

- Premium Coverage: Sometimes, "premium insurance" might be used colloquially to refer to insurance policies that offer high levels of coverage or additional benefits beyond basic or standard insurance plans. We offer more safety or extra features, such as increased coverage limits, a wider range of coverage, or other benefits like travel insurance or roadside assistance because these premium insurance plans frequently have higher premiums.

If you have a specific context or type of insurance in mind when referring to "premium insurance," feel free to provide more details, and I can offer a more tailored explanation.

- Write the main principles of insurance?

The main principles of insurance are:

- Principle of Utmost Good Faith (Uberrimae Fidei): Both the insured and the insurer are required to act in good faith and provide complete and accurate information to each other. In the insurance contract, this idea shows that it is very transparent and honest in the design and execution.

- Principle of Insurable Interest: The insured must have a financial interest in the subject matter of the insurance policy. This means that the insured must suffer a financial loss if the insured event occurs. Insurance contracts can't be utilized for speculation or gambling thanks to insurable interest.

- Principle of Indemnity: The principle of indemnity states that the insured should not profit from an insurance claim but should be restored to the same financial position they were in before the loss occurred. Insurance compensation is designed to compensate for the actual financial loss suffered, up to the limit of the policy.

- Principle of Contribution: If the insured has multiple insurance policies covering the same risk, each insurer will contribute proportionately to the loss. This principle prevents the insured from collecting more than the actual loss from multiple insurance policies, known as over-insurance.

- Principle of Subrogation: When an insurance company pays a claim to the insured, it gains the right to pursue legal action against any third party responsible for the loss. Subrogation allows the insurer to recover the amount paid to the insured and helps prevent the insured from collecting double compensation for the same loss.

- Principle of Loss Minimization: The insured has a duty to take reasonable steps to minimize the extent of the loss after an insured event occurs. If damages are not mitigated, the insurance provider may offer you less money.

These guiding ideas promote equality, accountability, and transparency in the insurance business By acting as the cornerstone of insurance contracts and a framework for interactions between insurers and insured parties.

- What is 4 and 8 in insurance?

In the insurance industry, "4 and 8" typically refers to the rule regarding payment of insurance premiums. It's more commonly known as the "Four and Eight Payment Plan."

The Four and Eight Payment Plan allows policyholders to pay their insurance premiums in installments, usually over four or eight equal payments. Policyholders who would rather not pay the full premium at once and instead spread it out over many months can do so with this arrangement, which provides flexibility.

For example, if an insurance policy has an annual premium of ,200, under the Four and Eight Payment Plan, the policyholder could pay it in four equal installments of 0 each or in eight equal installments of 0 each.

This payment plan is frequently available for a number of insurance policies, including renters', homeowners', and vehicle insurance. While preserving their insurance coverage it supports policyholders in efficiently managing their cash flow and spending plans.

- What is three types of insurers?

There are several kinds of insurers in the insurance business, and they all cater to distinct market niches and provide distinct kinds of insurance goods. Here are three common types of insurers:

- Stock Insurance Companies: Stock insurance companies are owned by shareholders who invest in the company's stock. When the business is making profit then the Shareholder gets return profits. Policyholders typically do not have ownership rights in the company. Property and casualty insurance, health insurance, life insurance, and other insurance products are just a few of the many products that stock insurance firms may provide.

- Mutual Insurance Companies: Mutual insurance companies are owned by their policyholders rather than external shareholders. Policyholders are considered members of the mutual company and may have voting rights and participate in the company's governance. Mutual insurers operate on a not-for-profit basis, with any profits generated being returned to policyholders in the form of dividends, lower premiums, or enhanced benefits. Mutual insurance companies often focus on providing life insurance, property and casualty insurance, or specialized insurance products.

- Reciprocal Insurance Exchanges: Reciprocal insurance exchanges, also known as interinsurance exchanges or reciprocal insurers, are unincorporated groups of individuals or entities that collectively insure each other's risks. Policyholders in a reciprocal insurance exchange pool their resources to provide insurance coverage to each other. Each policyholder is both an insured and an insurer, sharing in the risk and rewards of the exchange. Different kinds of insurance coverage, including liability, professional indemnity, and property and casualty insurance, may be available through reciprocal insurance exchanges.

These are only the three most typical kinds of insurance, but there are other variations and structures within the insurance industry, including captive insurance companies, government insurers, and reinsurance companies, among others. These are the type of insurance which has unique characteristics, advantages, and legal considerations.

- What are the 6 rules of insurance?

While there isn't a standard set of "6 rules of insurance," the principles and guidelines governing insurance are often summarized into several key principles or rules. Here's a compilation of six essential rules or principles of insurance:

- Utmost Good Faith (Uberrimae Fidei): Both the insured and the insurer are required to act in utmost good faith and provide complete and accurate information to each other during the formation and execution of the insurance contract. This idea guarantees openness, truthfulness, and justice in the insurance relationship.

- Insurable Interest: The insured must have a legitimate financial interest in the subject matter of the insurance policy. Insurable interest ensures that the insured would suffer a financial loss if the insured event occurs, preventing insurance contracts from being used for speculative purposes.

- Indemnity: The principle of indemnity states that insurance compensation should only cover the actual financial loss suffered by the insured, up to the limit of the policy. Insurance is intended to restore the insured to the same financial position they were in before the loss occurred, without allowing them to profit from the insurance claim.

- Contribution: If the insured has multiple insurance policies covering the same risk, each insurer will contribute proportionately to the loss. This principle prevents the insured from receiving more than the actual loss from multiple insurance policies, known as over-insurance.

- Subrogation: When an insurance company pays a claim to the insured, it gains the right to pursue legal action against any third party responsible for the loss. Subrogation allows the insurer to recover the amount paid to the insured and prevents the insured from collecting double compensation for the same loss.

- Mitigation of Loss: The insured has a duty to take reasonable steps to minimize the extent of the loss after an insured event occurs. If damages are not mitigated, the insurance provider may offer you less money.

These rules and principles form the foundation of insurance contracts and govern the relationship between insurers and insured parties, ensuring fairness, transparency, and accountability in the insurance industry.

Written By - Insurance Point Office

Created on 27 dec 2023 - Vehicle Insurance

Why Motor Insurance is needed in our daily life?

- Which vehicle insurance is best?

The "best" vehicle insurance is determined by taking into account a number of variables, such as your individual requirements, financial situation, available coverage, level of customer support, and the standing of the insurance provider. Here are some popular and reputable vehicle insurance providers that are often considered among the best:

-

ICICI Lombard General Insurance: One of the top general insurance providers in India, ICICI Lombard provides a variety of vehicle insurance plans. ICICI Lombard General Insurance is known for quick claim payment, and excellent customer service.

-

TATA AIG General Insurance: TATA AIG is known for its transparent policies, user-friendly online services, and prompt claim settlement process. TATA AIG General Insurance is known for quick coverage along with additional benefits such as roadside assistance and zero depreciation cover.

-

GO DIGIT General Insurance: GO DIGIT Assurance is a private-owned insurance company with a strong presence in the vehicle insurance sector. Go Digit General Insurance is known for quick insurance plans with flexible coverage options and competitive premiums.

-

RELIANCE General Insurance Company: Reliance Insurance is another private-owned insurance company that provides reliable vehicle insurance coverage. Reliance General insurance is known for quick cashless claim settlement and round-the-clock customer service for automobiles, motorcycles, and commercial vehicles.

Think about things like coverage options, cost-effectiveness of premiums, claim settlement history, level of customer service, and extra perks provided by the insurance provider when selecting the finest auto insurance for your requirements. To make an educated choice, it's recommended to evaluate many insurance choices, thoroughly study the terms and conditions of the policy, and, if necessary, speak with an insurance counselor.

- What is full insurance of vehicle?

"Full insurance" of a vehicle typically refers to a comprehensive auto insurance policy that provides extensive coverage against various risks and perils. It's also known as "comprehensive coverage" in some regions. Here's what is typically covered under a full insurance or comprehensive auto insurance policy:

-

Own Damage Coverage: Its provides protection against damages to your vehicle resulting from accidents, collisions, overturning, or other physical damage, regardless of fault.

-

Theft: Comprehensive insurance covers losses related to theft of the insured vehicle or its parts.

-

Vandalism: Damage caused by vandalism, such as graffiti or malicious acts, is typically covered under comprehensive insurance.

-

Fire: Comprehensive coverage extends to damages caused by fire, including vehicle fires and damages resulting from wildfires.

-

Natural Disasters: its includes coverage for damages caused by natural disasters such as floods, earthquakes, hurricanes, tornadoes, and hailstorms.

-

Collision with Animals: Damage resulting from collisions with animals, such as deer or livestock, is typically covered under comprehensive insurance.

-

Glass Damage: Comprehensive coverage usually includes coverage for repair or replacement of broken or damaged glass, such as windows and windshields.

-

Personal Belongings: Some comprehensive policies may provide coverage for personal belongings damaged or stolen from the insured vehicle.

-

Third-Party Liability: In addition to the above coverages, comprehensive insurance may also include third-party liability coverage, which protects you against legal liabilities arising from bodily injury or property damage caused to third parties in accidents involving your vehicle.

-

In this insurance policies deductibles, exclusions, and coverage restrictions might vary. For this reason, it's critical to thoroughly read the policy paperwork to determine what is and is not covered. Additionally, comprehensive coverage is usually optional and can be purchased as an add-on to a basic liability insurance policy.

Though wide protection is offered by comprehensive coverage, it's crucial to evaluate your specific demands and financial situation to decide if this is the best option for you. If you have a financed or leased vehicle, comprehensive coverage may be required by the lender or leasing company.

- What are the two types of car insurance?

The two primary types of car insurance are:

-

Third-Party Liability Insurance: Often referred to as liability-only insurance, third-party liability insurance covers injuries and damages your car may cause to other persons, their property, or other cars. It typically covers legal liabilities arising from accidents where you are at fault, including bodily injury to other parties and damage to their property. Third-party liability insurance is usually mandatory by law in many countries to drive a vehicle legally on public roads. However, it only covers damages to third parties and does not provide coverage for damages to your own vehicle.

-

Comprehensive Insurance: Comprehensive insurance, also known as full coverage or comprehensive coverage, provides broader protection than third-party liability insurance. In addition to covering damages and injuries caused to third parties, comprehensive insurance also covers damages to your own vehicle resulting from accidents, collisions, theft, vandalism, fire, natural disasters, and other covered perils. Comprehensive insurance offers more extensive coverage and financial protection for your vehicle but typically comes with higher premiums compared to third-party liability insurance.

-

These two kind of vehicle insurance meet various requirements and preferences. While third-party liability insurance provides basic coverage mandated by law, comprehensive insurance provides additional protection and peace of mind by covering a wider range of risks and perils. The ideal form of vehicle insurance must be selected after taking your particular demands, financial status, and risk tolerance into consideration. To further personalize your insurance policy according to your particular requirements, you may also think about adding endorsements or additional coverages.

Written By - Insurance Point Office

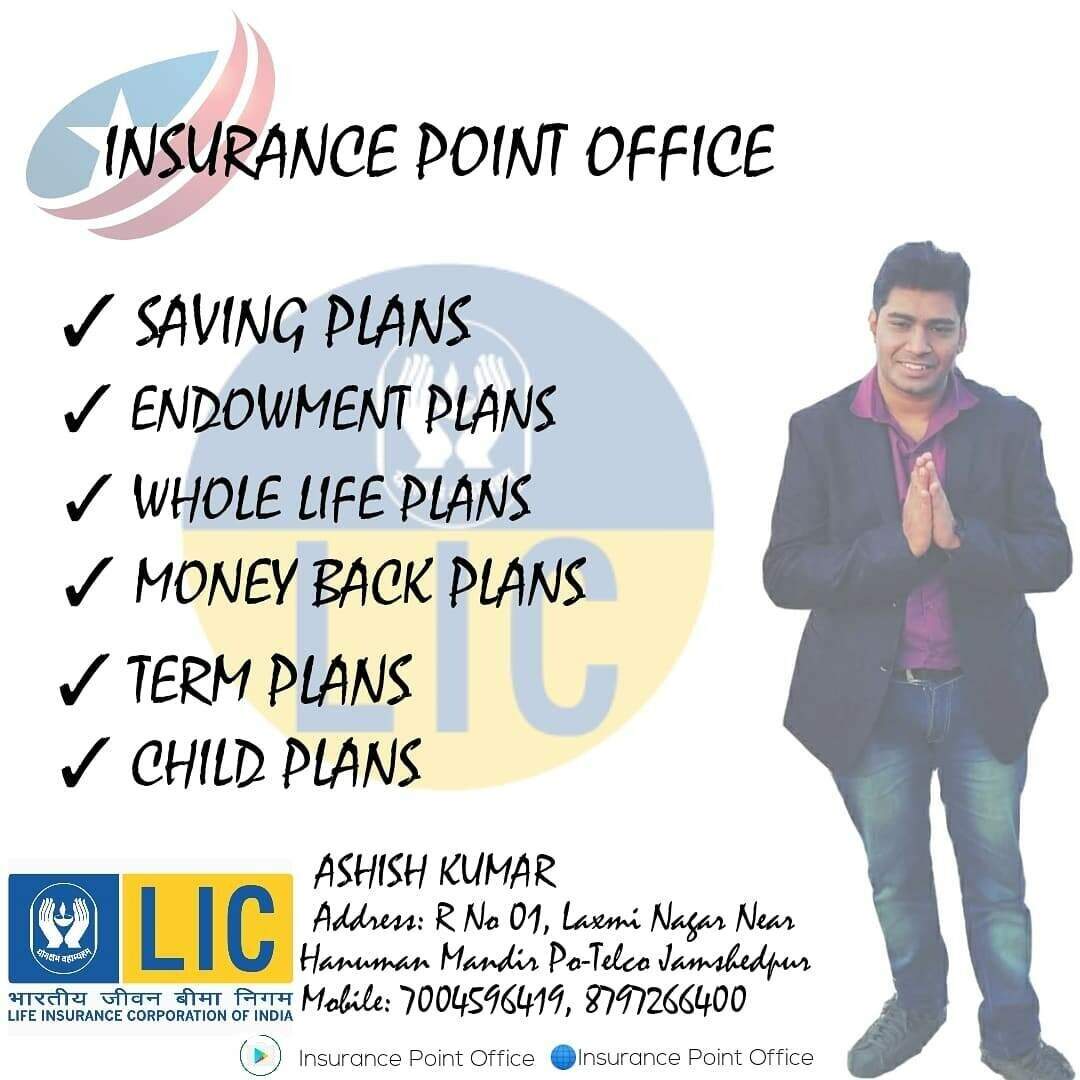

Created on 28 dec 2023 - life Insurance

Why life insurance is needed in your daily life?

- How can I check my LIC policy account?

To check your LIC (Life Insurance Corporation of India) policy account, you have a few options:

-

Online Portal: LIC has an online portal where policyholders can register and access their policy details. You can visit the LIC website and navigate to the 'Online Services' section. From there, you can register/login to your account and view your policy details, premium payment history, and other relevant information.

-

LIC Customer Portal: LIC also has a dedicated customer portal called LIC e-Services. You can register on this portal using your policy details and create an account. Once registered, you can log in to view your policy details, premium payment status, loan status (if applicable), and other policy-related information.

-

LIC Mobile App: LIC has a mobile app called 'My LIC' available for both Android and iOS devices. You can download this app from the respective app stores and log in using your policy details. We can also check services related to your LIC policies, including checking policy details, premium payment status, policy status, loan status, etc.

-

Through Agent/Branch: You can also visit your nearest LIC branch office or contact your LIC agent to inquire about your policy details. We provide you information and guidance regarding your policy account also.

Make sure to have your policy details handy when accessing your LIC policy account through any of these channels. If you encounter any issues or have specific queries, contacting LIC customer support would be advisable.

- How to calculate LIC maturity amount?

Calculating the maturity amount for an LIC (Life Insurance Corporation of India) policy involves considering various factors such as the sum assured, policy term, bonus (if applicable), and any additional benefits or riders attached to the policy. Here's a basic formula to calculate the maturity amount for an LIC policy:

-

Sum Assured: This is the amount guaranteed to be paid out at the maturity of the policy. It's the amount you're assured to receive provided you've paid all premiums as per the policy terms.

-

Bonus (if applicable): LIC may declare bonuses on participating policies. These bonuses accrue over the policy term and are usually declared annually or at the end of the policy term. Bonus rates vary depending on the type of policy and the performance of the insurance company. To calculate the bonus amount, multiply the bonus rate by the sum assured.

-

Final Addition Bonus (if applicable): In some policies, LIC may declare a final addition bonus at maturity. This is an additional bonus provided based on the overall performance of the insurance company and may be added to the maturity amount.

-

Additional Benefits/Riders (if applicable): If you've attached any riders or additional benefits to your policy, such as accidental death benefit or critical illness rider, the maturity amount may be affected accordingly.

The maturity amount may be determined using the following formula once you have all the necessary data:

Total Assured + Accrued Bonus + Final Addition Bonus + Additional Benefits/Riders (if applicable) = Maturity AmountTotal Assured + Accrued Bonus + Final Addition Bonus + Additional Benefits/Riders (if applicable) = Maturity Amount Remember that the actual maturity amount might change depending on your policy's terms and conditions, the insurance company's performance, and other elements. For an accurate calculation of your LIC policy's maturity amount, it's recommended to refer to your policy document or contact your LIC agent or customer support. You will able to get comprehensive details on your particular coverage.

- Is LIC government or private?

LIC (Life Insurance Corporation of India) is a government-owned insurance and investment company in India. It was established in 1956 by the Government of India when the Parliament of India passed the Life Insurance of India Act that nationalized the private insurance industry in India. Since then, LIC has been owned by the Government of India and operates as a public sector entity. In terms of the amount of life insurance business it handles, it is the biggest insurance firm in India and among the biggest worldwide.

- Why life insurance is importance?

Life insurance serves several important purposes:

-

Financial Protection: Life insurance provides financial protection to your family and dependents in case of your untimely death. The death benefit paid out by the insurance company can help replace lost income, pay off debts, cover living expenses, and maintain the standard of living for your loved ones.

-

Debt Repayment: Life insurance can be used to repay any outstanding debts such as mortgages, loans, or credit card debt, ensuring that your family does not inherit financial liabilities in the event of your death.

-

Income Replacement: If you are the primary breadwinner in your family, life insurance can replace your lost income, providing financial stability to your dependents and helping them meet their ongoing expenses and financial goals.

-

Education Funding: Life insurance proceeds can be earmarked to fund your children's education expenses, ensuring that they have the financial resources to pursue their educational aspirations even if you are no longer around.

-

Estate Planning: Life insurance can play a crucial role in estate planning by providing liquidity to cover estate taxes, settlement costs, and other expenses associated with the transfer of assets to beneficiaries.

-

Business Continuity: For business owners, life insurance can be used to fund buy-sell agreements, provide key person coverage, or ensure business continuity in the event of the death of a business partner or key employee.

-

Peace of Mind: Having life insurance coverage offers peace of mind, knowing that your loved ones will be financially protected and taken care of in your absence.

Written By - Insurance Point Office

Created on 30 dec 2023 - Health Insurance

Reasons Why You Should Get Health Insurance in Today’s Changing Times

- Which health insurance is the best?

The "best" health insurance plan will vary depending on a number of criteria, including personal preferences, healthcare provider network, budget, and individual needs. There isn't a universal solution because what suits one individual may not be the ideal choice for another. However, here are some considerations to help you choose a health insurance plan:

-

Coverage Needs: Assess your healthcare needs, including medical conditions, prescription medications, and anticipated medical services. Select a plan that offers sufficient coverage for the medical demands.

-

Network of Providers: Check if the health insurance plan has a network of healthcare providers, including hospitals, doctors, specialists, and pharmacies, that are conveniently located and accessible to you.

-

Costs and Premiums: Consider the coinsurance, copayments, deductibles, and premiums associated with the health insurance plan. To select a plan that fits your budget well, compare the prices of several options.

-

Coverage Options: Examine the alternatives for preventive care, emergency services, hospitalization, prescription medication, mental health services, and maternity care that are provided by the health insurance plan.

-

Financial Stability and Reputation: Research the financial stability and reputation of the health insurance company. Customer satisfaction surveys to assess the company's dependability and service quality while looking at reviews, ratings.

-

Additional Benefits: Wellness programs, telemedicine services, coverage for alternative medicine, and savings on medical services are just a few of the extra perks that some health insurance policies provide. Take into account these extra advantages while contrasting programs.

-

Policy Exclusions and Limitations: Read the policy documents carefully to understand any exclusions, limitations, or restrictions on coverage. Make sure that what is not covered by the health insurance plan and Make sure that what is covered.

-

Government Programs: If you qualify, research publicly funded health insurance plans such as Medicaid, which serves low-income individuals and families, and Medicare, which is available to seniors 65 years of age and older.

The ideal health insurance plan for you will ultimately rely on your unique objectives and circumstances. It's advisable to research and compare multiple health insurance options before making a decision. Additionally, consulting with a licensed insurance agent or broker can provide valuable guidance and help you navigate the complexities of health insurance.

- Which health insurance is best for claim?

A number of elements, including customer service, network of healthcare providers, claim settlement ratio, and convenience of the claim procedure, must be taken into account when choosing the best health insurance for claim purposes. Here are some health insurance companies in India known for their good claim settlement records and customer satisfaction:

-

Star Health and Allied Insurance: Known for its wide hospital network and quick claim settlement procedure, Star Health is one of the top health insurance carriers in India.

When choosing a health insurance plan, factors other than the claim settlement % should be taken into account. The hospital network, coverage options, premium prices, and client feedback are some of these variables. The terms and conditions, including exclusions and restrictions, to make sure the insurance meets your specific needs and expectations.

- What is benifits of having health insurance?

Financial protection against medical costs resulting from disease, accident, or other healthcare requirements is offered by health insurance. Its cover all healthcare services, including hospital stays, doctor visits, prescription medications, diagnostic tests, and preventative care.

Here's how health insurance works in healthcare:

-

Premium: Policyholders pay a premium to the health insurance company at regular intervals, typically monthly or annually. Age, health, available coverage are factors which affect this premium price.

-

Coverage: In exchange for the premium payments, the health insurance company provides coverage for specified healthcare services outlined in the policy. Pregnancy care, emergency care, outpatient services, inpatient hospitalization, and other medical procedures could all be covered.

-

Deductible: Many health insurance plans have a deductible, which is the amount that the policyholder must pay out-of-pocket before the insurance company starts covering medical expenses. Following the payment of the deductible, the policyholder is usually responsible for the remaining balance, with the insurance company covering a portion of the expenses (coinsurance or copayment).

-

Network of Providers: Health insurance plans often have a network of healthcare providers, including hospitals, doctors, specialists, and pharmacies, with whom they have negotiated discounted rates. Policyholders may receive full or partial coverage for services obtained within the network, and may have to pay higher out-of-pocket costs for services obtained outside the network.

-

Claim Process: When a policyholder seeks medical treatment covered by their health insurance policy, the healthcare provider submits a claim to the insurance company for reimbursement. The insurance company evaluates the claim based on the policy terms and, if approved, reimburses the healthcare provider for the covered services.

- Benefits: Health insurance provides financial protection against the high costs of medical care, helping individuals and families afford necessary healthcare services without facing significant financial hardship.

- Is Star Health Insurance good or bad?

- Claim Settlement Record: Check the claim settlement ratio of Star Health Insurance, which indicates the percentage of claims settled by the company compared to the total number of claims received. A higher claim settlement ratio typically indicates better reliability in honoring claims.

-

Coverage Options: Review the range of health insurance plans offered by Star Health Insurance and assess whether they align with your healthcare needs and budget. Consider the coverage limitations, perks, exclusions, and possible add-on options.

-

Network of Hospitals: Verify whether Star Health Insurance has a wide network of hospitals and healthcare providers in your area. Having access to a broad network can ensure that you receive timely medical care and benefit from cashless treatment facilities.

-

Customer Service: Research customer reviews and feedback about Star Health Insurance's customer service quality, responsiveness, and support during the policy purchase process, claim settlement, and other interactions.

-

Premium Affordability: Compare the premiums charged by Star Health Insurance with those of other insurance companies offering similar coverage. Evaluate whether the premiums are competitive and offer good value for the coverage provided.

- Policy Terms and Conditions: Make sure you understand what is and is not covered by carefully reading the terms and conditions of Star Health Insurance products, including coverage restrictions, waiting periods, pre-existing conditions, and exclusions.

In the end, how effectively Star Health Insurance satisfies your unique needs and expectations will determine whether you think favorably or poorly of it. Before choosing an alternative, it's a good idea to do a lot of research, weigh the pros and disadvantages of several insurance plans, and, if necessary, speak with a certified insurance expert. To select the best health insurance company for you, take into account additional aspects than reputation, such as policy features, perks, and level of customer service.

- Is Star Health owned by whom?

As of my last update in January 2022, Star Health and Allied Insurance Co. Ltd. is owned by a consortium of investors. This consortium includes top private equity companies including WestBridge Capital, Madison Capital, and Sequoia Capital, among others. These investors bought a big interest in Star Health Insurance in a transaction that occurred in 2018. It's crucial to note that ownership structures can change over time due to a number of factors, including mergers, acquisitions, and changes in ownership interests. Therefore, for the most current information on the ownership of Star Health Insurance, I recommend consulting recent financial reports, company announcements, or reliable news sources.

- What is the minimum amount for Star Health Insurance?

The minimum amount for Star Health Insurance, like any health insurance plan, can vary depending on several factors, including the type of plan, coverage options, age of the insured, and other individual factors. However, typically, health insurance plans have a minimum premium amount that policyholders need to pay to obtain coverage.

For Star Health Insurance, the minimum premium amount can depend on the specific health insurance product you choose and the coverage options selected. Individual health insurance plans, family health insurance plans, senior citizen health insurance plans, and group health insurance plans offered by Star Health Insurance may have different minimum premium amounts.

To determine the minimum premium amount for Star Health Insurance, it's advisable to contact Star Health Insurance directly or visit their official website to explore their various health insurance products and request a quote based on your specific requirements and preferences. Age, medical history, sum insured, and coverage restrictions can all have an impact on a health insurance policy's premium. Therefore, whether seeking a pricing estimate from Star Health Insurance or any other health insurance provider, it is imperative that you provide correct information.

Written By - Insurance Point Office

Created on 30 dec 2023 - Insurance Advisor

Why people need a insurance advisor?

-

Is an insurance advisor a good job?

A person's interests, abilities, and professional objectives are just a few of the variables that determine whether or not being an insurance advisor is a successful job. Here are some considerations to help you assess whether becoming an insurance advisor is a good fit for you:

-

Flexibility: Being an insurance advisor often offers flexibility in terms of work hours and schedule. You might be able to choose your own hours and work from anywhere, including your home or while on the road.

-

Income Potential: Insurance advisors typically earn commissions and bonuses based on the policies they sell and the premiums generated. The financial potential can be substantial, particularly if you are able to develop a sizable clientele and close a lot of policies.

-

Helping Others: As an insurance advisor, you have the opportunity to help individuals and families protect themselves financially by providing them with appropriate insurance coverage tailored to their needs. Knowing that you are raising people's quality of life could be completed by helping them lower risks and secure their future.

-

Continuous Learning: The insurance industry is dynamic and constantly evolving. For insurance advisor its essential to Keeping up with changes in insurance products, regulations, and market developments. If you appreciate learning new things and being up to date on financial goods and services, this part of your employment may be interesting. Prospective Networking: Establishing connections with customers, insurance providers, and other industry experts can yield significant prospects for networking. You have to Increasing your insurance sector relationships To build your clientele, expand your business, and enhance your professional position.

-

Challenges and Competition: Like any sales-oriented job, being an insurance advisor comes with its challenges, including competition from other advisors, meeting sales targets, and handling rejection.

-

Regulatory Requirements: Depending on your location and the type of insurance products you sell, you may need to obtain licenses or certifications to work as an insurance advisor. Maintaining your trust and legality in the business requires being up to date on regulatory regulations and compliance standards.

All things considered, for people who like helping others, have excellent interpersonal and sales skills, and are prepared to put in the work to establish and sustain client relationships, becoming an insurance adviser may be a gratifying and financially rewarding job. You should know the role's requirements, review your abilities and interests, and determine whether it is a good fit for you or not Before choosing a job as an insurance advisor.

-

How does insurance advisor earn?

Insurance advisers, often known as insurance agents or brokers, are generally compensated through commissions and incentives depending on the insurance policies they sell and the premiums collected. Here's how insurance advisors earn:

-

Commissions: Insurance advisors receive commissions from insurance companies for each policy they sell. The commission amount is usually a percentage of the premium paid by the policyholder. The commission rate may vary depending on the type of insurance policy, the insurance company, and other factors. Commissions can be paid as an upfront lump sum or as ongoing payments over the duration of the policy (renewal commissions).

-

Bonuses: In addition to commissions, insurance advisors may also earn bonuses and incentives from insurance companies based on their performance, such as meeting sales targets, achieving certain production levels, or selling specific insurance products. Additional revenue and prizes to high-performing advisers are given as a bonuses.

-

Renewal Commissions: For insurance policies that have renewal premiums, insurance advisors may continue to earn commissions on the policy's renewal premiums as long as the policy remains in force. Renewal commissions give continued revenue to advisers for the life of the insurance term.

-

Cross-Selling and Upselling: Insurance advisors may have the opportunity to earn additional income by cross-selling or upselling other insurance products or services to existing clients. For example, an advisor who sells auto insurance may also offer home insurance, life insurance, or other types of insurance coverage to the same client, earning additional commissions on those sales.

-

Contingent Commissions: Some insurance companies offer contingent commissions or profit-sharing arrangements to insurance advisors based on the overall profitability of the business written by the advisor or agency. These contingent commissions are typically paid out annually or periodically based on predefined performance metrics and profitability targets.

-

Fee-Based Services: In addition to earning commissions from insurance sales, some insurance advisors may offer fee-based services, such as financial planning, risk management consulting, or insurance advisory services, for which they charge clients a fee separate from the insurance premiums. This fee-based approach allows advisers to diversify their income streams while also providing extra value-added services to their customers.

The volume and kind of insurance policies sold, the commission rates offered by insurance firms, the advisor's performance and sales abilities, and the level of competition in the insurance market are some of the factors that might affect an advisor's overall earnings.

In addition to offering their clients essential insurance products and services, a prosperous insurance consultant may earn a substantial income from commissions, bonuses, and other benefits.

-

What is the difference between insurance agent and advisor?

Although the phrases "insurance advisor" and "insurance agent" are sometimes used interchangeably, their meanings might vary somewhat according on the situation. Here's the typical distinction between the two:

-

Insurance Agent:

- An insurance agent is a licensed professional who represents one or more insurance companies and sells insurance products and services on behalf of those companies.

- Insurance agents typically work directly for an insurance company or are affiliated with an insurance agency or brokerage.

- Insurance products such as life, health, vehicle, and property and casualty insurance might be the focus of an agent's specialization.

- The main goals of agents are to distribute and sell insurance products.

- Based on the insurance policies they sell and the premiums they produce, agents are paid commissions and incentives.

-

Insurance Advisor:

- An insurance advisor is a broader term that encompasses professionals who provide advice, guidance, and expertise on insurance-related matters to individuals, businesses, or organizations.

- Insurance brokers, consultants, financial planners, and other experts providing insurance-related services can also be considered insurance advisers in addition to insurance agents.

- All financial counsel and planning, including insurance, risk management, retirement, investment, and estate planning our done by advisor.

- Always check that policy should have maximum risk coverage, and financial objectives before offering appropriate insurance choices for their specific situations.

- Insurance advisors may work independently or as part of a financial advisory firm, insurance brokerage, or wealth management firm.

- Insurance consultants may charge for their advisory services in addition to receiving commissions from insurance sales, such as fees for financial planning or advising.

Conclusively, insurance advisors provide broader financial guidance and support, encompassing insurance planning, as part of a comprehensive financial planning procedure, whereas insurance agents often focus on marketing insurance products on behalf of insurance companies. Depending on their unique job activities and the services they provide, insurance agents and advisers may have overlapping tasks and responsibilities.

-

What is the qualification for insurance agent?

The criteria for becoming an insurance agent differ by nation and the unique legislation regulating the insurance sector in that jurisdiction. However, here are some general credentials and actions commonly necessary to become an insurance agent:

-

Educational Requirements: In many countries, a high school diploma or equivalent is the minimum educational requirement to become an insurance agent. Some insurance companies may prefer candidates with a college degree or relevant coursework in business, finance, economics, or related fields.

-

Licensing: Insurance agents must obtain a license from the regulatory authority or insurance department in the state or country where they intend to sell insurance products. One must complete pre-licensing coursework, pass a licensing test, and fulfill other eligibility requirements including background checks to obtain a license.

-

Pre-Licensing Education: Candidates for insurance agent licensure are usually required to complete a specified number of hours of pre-licensing education courses approved by the regulatory authority.

-

Licensing Exam: After completing the pre-licensing education requirements, candidates must pass a licensing exam administered by the regulatory authority or an approved testing provider. The test evaluates a candidate's understanding of insurance principles, legal requirements, and moral principles.

-

Background Check: Insurance agent candidates may be subject to background checks, including criminal history checks and financial background checks, as part of the licensing process. Certain criminal convictions or financial issues may disqualify individuals from obtaining an insurance license.

-

Continuing Education: After obtaining a license, insurance agents are typically required to complete continuing education courses on an ongoing basis to maintain their license. Requirements for continuing education make ensuring that agents are up to date on modifications to insurance laws, rules, goods, and market trends.

-

Appointment by Insurance Company: In addition to obtaining a license, insurance agents must be appointed by one or more insurance companies to represent them and sell their insurance products. Appointment requirements may vary depending on the insurance company's policies and procedures.

If someone wants to work as an insurance agent, they must adhere to all legal requirements and conduct study on the particular licensing processes and regulations in their country. Insurance agents may find that developing their sales skills, strong interpersonal and communication qualities, and in-depth understanding of insurance products and services are all beneficial for success in the field.

- What are the insurance agents duties?

As go-betweens for clients and insurance firms, insurance agents are essential to the insurance sector. When it comes to sales, customer service, and compliance it has broad variety of responsibilities. Here are some common duties of insurance agents:

- Sales and Marketing:

- Prospect for potential clients through various channels, such as cold calling, referrals, networking, and lead generation activities.

- Inform customers on benefits, rates, coverage alternatives, and insurance products.

- Risk profiles of clients to recommend suitable insurance solutions and assess the insurance needs.

- Present insurance ideas, quotations, and negotiate terms to fit the client's needs.

- Close sales and facilitate the purchase of insurance policies, ensuring all necessary paperwork is completed accurately and promptly.

- Customer Service:

- Help customers with insurance modifications, updates, and endorsements, such as adding or eliminating coverage, changing contact information, or altering policy limits.

- Process insurance applications, policy renewals, cancellations, and reinstatements in accordance with company policies and procedures.

- Clients can receive assistance with concerns regarding their claims, be guided through the process, and have an advocate working to ensure a fair and timely reimbursement.

- Relationship Building:

- Developing Relationships: Get to know your clients' insurance requirements, preferences, and any life events that could affect those needs.

- Good communication is basic. Listen actively, express yourself clearly, and show empathy.

- Regularly follow up with clients to give further assistance, policy evaluations, and chances for upselling or cross-selling more insurance products.

- Compliance and Ethics:

- Adhere to ethical standards and professional conduct guidelines set forth by regulatory authorities and industry associations.

- Assure adherence to all relevant laws, rules, and license specifications controlling the insurance sector.

- Minimizing operational, financial, and reputational risks.

- Fostering a positive work environment where employees feel valued and respected.

- Professional Development:

- Continuously update knowledge and skills related to insurance products, sales techniques, customer service best practices, and industry developments through training programs, seminars, workshops, and self-study.

- Identifying and developing specific skills relevant to your profession or career goals. This could range from technical skills (e.g., programming languages, design tools) to soft skills.

- Is insurance agent a profession?

Yes, being an insurance agent is considered a profession. A paid job requiring specific training, knowledge, abilities, and ability in a particular sector is sometimes referred to as a vocation. These requirements are met by insurance agents since they complete specialized training, get the necessary licenses, and gain knowledge of insurance services and products to help customers with their insurance needs.

Here are some reasons why being an insurance agent is considered a profession:

- Specialized Training: Insurance agents undergo training and education to acquire knowledge about insurance principles, products, laws, regulations, sales techniques, and customer service practices. They often complete pre-licensing courses and pass licensing exams to obtain the necessary qualifications to work as insurance professionals.

- Licensing Requirements: Insurance agents are required to obtain licenses from regulatory authorities or insurance departments in the jurisdictions where they operate. Agents who get licenses are guaranteed to fulfill specific competency criteria and adhere to ethical and legal obligations in order to operate as insurance professionals.

- Expertise and Skills: Insurance agents learn and develop skills in a range of insurance-related areas, including risk assessment, policy analysis, salesmanship, negotiation, communication, and client relationship management. to educate clients, recommend suitable insurance plans, and provide top-notch client support we have to educate them.

- Client-Centric Approach: Insurance agents serve as trusted advisors to clients, helping them understand their insurance needs, explore coverage options, and make informed decisions to protect their financial interests And they work to build lasting client relationships through quality service based on trust, integrity, and professionalism.

- Ethical Standards: Insurance agents are expected to adhere to ethical standards and professional conduct guidelines established by regulatory authorities, industry associations, and professional codes of ethics. They are committed to serving the interests of their customers and to maintaining the confidentiality of their customers and will display conduct respectful of all with uplifted integrity and honesty in every contact.

To stay a successful insurance agent and fulfill their obligations in a way that appropriately addresses customers' insurance needs, an interdisciplinary blend of technical competence, abilities, professionalism, and ethical behavior are required for insurance job.

Written By - Insurance Point Office